Over the last several months, we’ve been working on a new investment presentation that outlines WJ’s approach to portfolio management, from start to finish. This will cover everything from the most basic ideas like what is a benchmark, to the technical strategies that optimize a portfolio.

We believe that the more informed the client is about what is going on in their portfolio, the better. There is no tactic, strategy, or philosophy in our process that we think client’s “can’t handle” or “don’t need to understand”. It’s like when you go to a great restaurant, the kitchen is often open to its customers, so they can see and understand what goes on in preparing their food. We’d be more worried about the restaurant who fears customers see what goes on behind the curtain.

As such, we will be delivering this presentation to all of our clients personally over the next year. This blog serves as a preview of the broader framework we’ll share in our presentation, and we can get into more of the specifics when we meet in person.

Where to Start

If you’re creating a portfolio for the first time, which of these would you purchase and at what weight?

US Stocks, foreign stocks, treasury bonds, corporate bonds, mortgage-backed securities, TIPS, real estate, commodities, currencies, crypto, private equity, private credit, hedge funds, REITs, MLPs..?

Talk about selection paralysis. That doesn’t even begin to scratch the dozens of strategies hedge funds implement, or the types of stocks, commodities or real estate there are to choose from. We need somewhere to start.

Fortunately, the market does this for us. If markets broadly reflect the collective wisdom of all investors, the most “neutral” starting point is the global market portfolio, which is the sum of every investor’s portfolio worldwide. This is somewhat theoretical as it's hard to measure everything investors hold, but we can get close. After filtering out most private investments and residential real estate, Goldman Sachs estimates the global market portfolio as below:

Simplified, it’s roughly:

Simplified, it’s roughly:

-

~50% global stocks

-

~37% bonds

-

~13% everything else (private markets, real estate, gold, crypto, etc.)

For liquidity and practicality, we focus primarily on stocks and bonds, which simplifies to something close to a global 60/40. This is our starting point and gives us a historical risk and return profile that we can build on after the client establishes their benchmark.

Creating Benchmarks

The global portfolio is a useful starting point, but not the right portfolio for everyone. Each investor’s benchmark should reflect:

-

Risk tolerance

-

Withdrawal needs

-

Horizon and stage of life

-

Personal financial goals

The chart below is a helpful way to visualize the risk/return tradeoff between any combination of stocks and bonds. Below we plot the global market portfolio discussed above, as well as the three primary WJ benchmark combinations. Your benchmark should be the point on that line that best fits you. Do you want to grow faster, but with more bumps in the road? Go towards the right on the chart, and vice versa.

Benchmarks are crucial to the investment management space, and without one you are investing blindly.

Benchmarks are crucial to the investment management space, and without one you are investing blindly.

Benchmarks serve multiple functions at WJ, including:

-

They provide a performance evaluation standard.

-

They establish a risk level clients agree to accept.

-

They guide investment strategy formulation.

-

They enhance transparency and facilitate clear communication with clients.

-

They provide the ability to set expectations by analyzing the past.

The Goal of Active Portfolio Management

Once the benchmark is set, our goal as portfolio managers is to improve on it. We do this by adding or subtracting different investments/strategies from the benchmark.

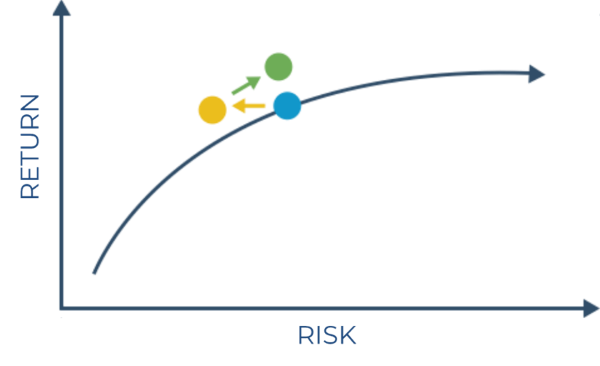

Visually, the goal is always the same when we deviate from the benchmark: move the portfolio up and/or to the left on the risk/return chart, more return, less risk.

Visually, the goal is always the same when we deviate from the benchmark: move the portfolio up and/or to the left on the risk/return chart, more return, less risk.

Most portfolio decisions we are able to make are to try and affect the portfolio in one of two ways:

- Reduce Risk

- Increase Returns

It’s rare for a single allocation decision to do both simultaneously, though not impossible. Most decisions lean clearly toward one or the other, which we’ll break apart below.

It’s rare for a single allocation decision to do both simultaneously, though not impossible. Most decisions lean clearly toward one or the other, which we’ll break apart below.

Reducing Risk

We have a variety of tools and tactics we can use to try and reduce risk from the benchmark. We list several below:

-

Diversifying Alternatives

Harry Markowitz, known as the father of modern portfolio theory, showed in 1952 that diversification is not “owning many things,” but owning things that don’t move together. When we’re evaluating an alternative, we are looking for strategies that have:

-

A positive track record

-

An economic rationale for why it should continue to be positive (many old strategies quit working)

-

Low correlation to stocks or bonds

Examples of strategies that meet those criteria are:

-

Managed futures

-

Reinsurance

-

Global macro

-

Market neutral

-

Some tactical strategies

There are many that meet 2 of the 3 criteria, but surprisingly few that are 3 for 3.

True diversification also requires understanding the risk drivers for a strategy, not just historical correlations. It’s part science and math, part intuition on how certain risks should correlate in the future.

-

Increasing Credit Quality in Bonds

A “AAA-rated” bond is safer than a “CCC-rated” bond. Of course, the yield you are paid is lower as well, but this is an easy lever we can pull to reduce risk.

-

Adding Duration (longer maturity bonds)

Duration is a measure of how sensitive your bond prices are to changes in interest rates. Long-term Treasuries generally have the highest duration, which often helps when in a crisis. They’re not perfect, 2022 reminds us that inflation can break the relationship, but historically they’re great diversifiers to stock risk.

-

Reducing Beta (aka equity risk)

You can lower equity risk by either reducing stock for something less risky or by keeping the same weight, but holding more defensive stocks (for example, shifting from Tesla to Procter & Gamble). Same goal, two approaches.

-

Rebalancing

Systematically selling recent winners and buying laggards to maintain target weights. This is far more powerful than most investors realize, especially in well diversified portfolios where return paths diverge meaningfully.

Enhancing Return

While reducing risk is important, it’s almost always at the cost of return. The following tactics seek to improve return, often by accepting more risk, but sometimes by exploiting structural inefficiencies:

-

Equity Factor Investing

Tilting equities toward characteristics like value, momentum, quality, etc. Historically, these have delivered excess returns beyond what simple market exposure explains. We wrote recently about factors here.

-

Reducing Credit Quality in Bonds

The opposite of increasing quality started earlier. There are times where it makes sense to buy bonds from lower credit quality issuers.

-

Tactical Asset Allocation

A fancy term for market timing. We generally caution against this as a fool’s errand. However, there are systematic, rules-based strategies using trend, valuation, or risk signals that have been shown to add value when done with discipline over time.

-

Private Alternatives

Private equity, private credit, and private real estate have historically offered higher returns than public markets. But despite their “smooth” reported volatility, the underlying risk from leverage, illiquidity, and lower credit quality is often higher.

-

Capital Efficiency (aka Leverage)

Capital efficiency is the ability to use different types of leverage to maximize exposure with less capital. For example, there are several tools today that allow investors to get $2 of exposure to certain assets for $1. This can be done in a variety of ways, but often it’s with the use of derivatives, such as futures contracts. We use controlled leverage to calibrate the portfolios risk to our desired target.

Putting It All Together

All these tools exist to serve one goal: create a better version of the benchmark that matches the same risk level but delivers higher expected return.

Again, we can think about it in two steps:

-

Reduce risk as much as possible without straying too far from the benchmark.

-

Add return enhancers until the risk rises back to the original target, but now with better expected performance.

This keeps the portfolio aligned with the client’s needs while still striving for improvement.

What We Don’t Do

We avoid decisions that add risk without adding value:

-

Chasing yield over total return

-

Speculating in assets with no fundamental value

-

Overpay for commoditized strategies.

-

Chasing fads or stories

-

Over-concentrating in any individual position

-

Selling in drawdowns (we’re more likely the ones buying)

-

Hiring or firing managers based solely on recent performance.

These behaviors destroy wealth far more reliably than they build it.

In our upcoming presentation, we’ll walk through the full WJ investment framework. But the big idea is simple:

Every investment decision links back to two goals: enhance return or reduce risk.

It’s a clear and intuitive way to think about a complex process. There’s plenty more beneath the surface, but no matter the level of complexity, the decision always comes back to how it moves the portfolio on the risk return line. We look forward to going into more detail with all of you. As always, if you have questions please give us a call.

PAST PERFORMANCE IS NOT A GUARANTEE OF CURRENT OR FUTURE RESULTS. Examples of historical information included in this presentation do not, nor are they intended to, constitute a promise of similar future results. Specific client portfolio allocations, risks and returns can and may deviate from these examples depending on accounts and types of investments available through each account. Future market views by WJ Interests, LLC may vary significantly from the historical examples presented herein and no one receiving this summary should assume that WJ Interests, LLC will be able to replicate successful views in the future.